Celebrating Tax Season Survival: What’s Next for Your Small Business Finances?

Tax season is finally behind us, and for small business owners, that often means a sigh of relief. But as you catch your breath, it's important to shift your focus from past filings to future financial strategies before time gets away from you. Here are some key steps...

Understanding Business Credit Scores and How to Improve Yours

As a small business owner, you're likely familiar with the concept of personal credit scores and how they can impact your financial life. But did you know that your business also has its own credit score? Your business credit score plays a crucial role in your ability...

Understanding Small Business Loans and Financing Options

Are you a small business owner seeking financial support to start, expand, or maintain your business operations? Understanding the various types of small business loans and financing options available can be crucial. Here, we'll explore some common options, their...

The Sunsetting of the Tax Cuts & Jobs Act: What Small Businesses Need to Know

The Tax Cuts and Jobs Act (TCJA), signed into law in December 2017, brought significant changes to the U.S. tax code. Among its many provisions were tax cuts for individuals and corporations, which were particularly beneficial for small businesses. However, it's...

Year-End Financial Statements: Why They Matter for Your Business

As the year comes to a close, business owners have a lot on their plates. There are holiday sales to manage, year-end bonuses to distribute, and the excitement of planning for the new year ahead. Amidst all this hustle and bustle, it's easy to overlook a critical...

Maximizing Your Small Business Impact: Giving to Charities & Nonprofits

As a small business owner, you understand the importance of making every penny count. But did you know that giving to charities and nonprofits can not only make a positive impact on your community but also offer significant tax benefits? Learn how strategic giving can...

Stitely & Karstetter CPAs Embarks on a New Chapter as SK CPAs & Business Advisors PLLC

In an exciting evolution, Stitely & Karstetter CPAs has unveiled its transformation into SK CPAs & Business Advisors PLLC. This significant change isn't limited to just a name adjustment — a vibrant new logo and a fully revamped website complement the new...

Stitely & Karstetter CPAs Evolves into SK CPAs & Business Advisors PLLC

Update showcases new branding, enhanced digital presence, and specialized business focus [Chantilly, Virginia, October 20, 2023] – In a landmark move that signifies growth, evolution, and a sharpened focus, Stitely & Karstetter CPAs is proud to announce its...

Run Your Business with More Clarity – Outsourced CFO Benefits

Run Your Business with More Clarity – Outsourced CFO Benefits As a business owner, managing finances and making informed financial decisions are crucial for long-term success. However, few small businesses can afford a full-time Chief Financial Officer (CFO). That's...

Protecting Your Small Business: Essential Tips to Avoid Financial Fraud

Financial fraud poses a significant threat to small businesses, as it can lead to severe financial losses, damaged reputations, and even business closure. As a small business owner, it is crucial to prioritize safeguarding your finances from fraudulent activities....

IRS Audits Likely to Increase Due to Inflation Reduction Act

The IRS has been given an unprecedented budget of $80 billion under the Inflation Reduction Act, which was passed in August 2022. This funding will go towards enhancing taxpayer services, enforcement, operational support, and business systems modernization. Most...

Small Businesses Benefit From Offering 401(k) Plans

Have you been considering creating a 401(k) plan as part of your employee benefits package but aren’t sure if it’s the right move? Offering a 401(k) plan to employees can be a good idea for small businesses for several reasons: Attract and retain top talent: Offering...

Standard Mileage Rates Increase in 2023

Business owners will be able to deduct three cents more per mile in 2023 when operating vehicles for business use, according to the Internal Revenue Service (IRS). The IRS recently announced the 2023 optional standard mileage rates used to calculate the deductible...

Stitely & Karstetter Promotes Max Spracklin to Partner

Chantilly, Virginia-based accounting firm SK CPAs & Business Advisors PLLC (S&K), PLLC, announced that Max Spracklin has been named a partner in the firm. Spracklin joined S&K in August 2016 after earning his BBA in Accounting from Radford University. As...

Small Business Pension Plans: What is the Right Fit for Your Business?

Are you ready to offer a pension plan to your employees but not sure where to start? Join the team at SK CPAs & Business Advisors PLLC January 19 at 3 p.m. at the Capital Grille in Fairfax for a free seminar: Small Business Pension Plans: What is the Right Fit for...

New Process For Claiming Electric Clean Vehicle Credit

[kc_row use_container="yes" _id="775554"][kc_column width="12/12" video_mute="no" _id="783055"][kc_column_text _id="430790"] In order to reduce carbon emissions and invest in the energy security of the United States, the Inflation Reduction Act of 2022, signed into...

Significant Tax Credit For Business Owners Who Purchase Electric Vehicles

Business owners who purchase electric vehicles will be able to take advantage of a new tax credit worth up to $40,000 next year. Last August, President Joe Biden signed The Inflation Reduction Act, which incentivizes purchasing electric cars, trucks, and other...

Client Appreciation Shred Event & Tailgate Saturday, November 5

Client Appreciation Shred Event & Tailgate Saturday, November 5 11 a.m.-2 p.m. Are boxes of old documents and sensitive materials cluttering up the corners of your home or office space? Need a place to dispose of them safely? Then Stitely and Karstetter’s...

Charity Golf Tournament Benefiting Paws of Honor Friday, October 28

Charity Golf Tournament Benefiting Paws of Honor Friday, October 28 9:30 a.m.-12:30 p.m. Please join SK CPAs & Business Advisors PLLC for our Annual Charity Golf Tournament as we tee off in style in private full-service bays at Top Golf One Loudoun. This year,...

New Virginia Tax Rebate: Are You Eligible?

If you are a Virginia resident, you may be eligible for a new Virginia tax rebate. According to Virginia Tax, an agency of the Commonwealth of Virginia, the 2022 Virginia General Assembly passed a law earlier this year giving taxpayers with a liability a rebate of up...

Stitely and Karstetter Sponsor Third Annual Charity Golf Tournament

On Friday, October 28, 2022, Stitely and Karstetter will sponsor their third annual charity golf tournament at TopGolf in Ashburn, VA. All proceeds raised will benefit the non-profit, “Paws of Honor,” which supports our nation’s retired military and law enforcement...

S&K’s New Tax Resolution Services Division Offers IRS Assistance

Are you in trouble with the IRS and don’t know where to turn? Even if you are not a current client, Stitely and Karstetter (S&K) can help! The firm recently announced the opening of its new Tax Resolution Services division in response to a growing need for...

Do You Qualify for Employer Retention Credits?

Do You Qualify for Employer Retention Credits? For a separate charge unrelated to your Total Accounting Care fee, the Stitely and Karstetter (S&K) team can meet with you to offer guidance on the requirements to qualify, as well as file your tax credit application....

Economic Injury Disaster Loan Repayments

[kc_row _id="984448"][kc_column _id="773033"][kc_column_text _id="871286"]Economic Injury Disaster Loan Repayments If your small business set up an Economic Injury Disaster Loan (EIDL), whether related to a natural disaster or COVID-19, it’s important that you set up...

Handling Foreign Assets

Handling Foreign Assets Do you hold foreign assets outside of the United States? Under the Foreign Account Tax Compliance Act (FATCA), US taxpayers holding financial assets outside the country must report those assets to the IRS using Form 8938, Statement of Specified...

IRS Announces Mid-year Increases in Mileage Rates

[kc_row use_container="yes" force="no" column_align="middle" video_mute="no" _id="334586"][kc_column width="12/12" video_mute="no" _id="329218"][kc_column_text _id="824931"] If you deduct mileage on your taxes, you will want to be aware of a recent increase in...

Tax Planning for Wage Earners

This time of year, people often ask me, “Frank, it seems like I pay a lot in taxes. What can I do to pay less?” Mostly, they are really asking me, “How can I save on taxes by moving some numbers around on paper?” To save on taxes, our elected representatives strike a...

Special Tax Rules for Rehiring Staff

If you find yourself short-staffed, one quick fix may be calling a former employee who has retired. You won't jeopardize your pension plan's tax status if you rehire retirees, nor is it a problem if you permit distributions of retirement benefits to employees who hit...

Thanks For Helping Us Help You This Tax Season

Tax season has come and gone, and we are finally able to take a breath. We would like to extend our deepest gratitude to all our clients for working so quickly and efficiently with us during the 2022 tax season. By thoroughly reading our emails and blog posts,...

Thanks For Helping Us Help You This Tax Season

[kc_row use_container="yes" force="no" column_align="middle" video_mute="no" _id="799321"][kc_column width="12/12" video_mute="no" _id="146334"][kc_column_text] Tax season has come and gone, and we are finally able to take a breath. We would like to extend our deepest...

Filing the Final Tax Return as an Executor

As a survivor, executor or administrator of an estate, you are obligated to file an income tax return reporting all the deceased's income up to his or her date of death. You will need to be aware of all the credits and deductions the deceased is allowed, as if that...

Keep These Important Tax Deadlines Top-of-Mind

Here at Top Level Accounting, we are continuing to work hard to prepare your tax returns. Please don’t forget about the following important deadlines: The deadline for personal tax documents to be sent to us, in order to avoid filing an extension, is March 20....

It’s Tax Season – Let’s Get Started

It's Tax Season ... Let's Get Started If you would like us to prepare a C-Corporation, S-Corporation or Partnership return, the best time frame to deliver your paperwork to our office or upload documents to the Client Center is ASAP. Our deadline for receiving...

Access Our Client Center for Tax Related Information

‘Tis the season…tax season, that is! In order to help you best prepare to file on time, we encourage you to frequently check our client center, as we continually will be posting information about taxes. We most recently uploaded engagement letters for 1099s, which...

TAC to Prepare 1099 Forms for All Clients in Early January

Clients Asked to Submit All W9’s to TAC, Via Client Center, by Saturday, 1/15 Happy Holidays from your friends at Total Accounting Care! Christmas is almost here, and soon we’ll be ushering in a brand new year. This means that TAC will...

S&K Sponsors Charity Golf Event, Raises $3,000 for Paws of Honor

On Thursday, October 21, Stitely and Karstetter CPA’s sponsored our second annual charity golf event. Held at Top Golf in Ashburn, Virginia – the event successfully raised nearly $3,000 for Paws of Honor, a local charity that provides free veterinary care and products...

Total Accounting Care Welcomes New Staff Accountant, Janisha Watkins

On October 18, Total Accounting Care proudly welcomed Janisha Watkins to our team. Janisha joins TAC as a staff accountant, after working in the accounts departments of several local non-profits. While she currently resides in Herndon,...

Total Accounting Care Welcomes Edd Dugbartey

Total Accounting Care is pleased to welcome a new member to our team - Edd Dugbartey, who joined our enterprise on October 18 as a staff accountant. Edd is currently in training, and will be assisting TAC clients with reconciling, bookkeeping and tax...

S&K Hosts Successful Shredding Event

On Saturday, October 16, Stitely and Karstetter hosted another successful shredding event at our offices for more than 50 attendees, including clients and friends of the company. Lunch was served, as well as beer and wine from local breweries and wineries. Hundreds of...

Stitely and Karstetter Sponsors Annual Golf Tournament on October 21 All proceeds raised will benefit “Paws of Honor” charity

On Thursday, October 21, Stitely and Karstetter will once again sponsor their annual charity golf tournament at TopGolf in Ashburn, VA. All proceeds raised will benefit “Paws of Honor,” which supports our nation’s retired military and law enforcement dogs. All...

TAC’s Parent Company, Stitely and Karstetter, to Sponsor Annual Golf Tournament on October 21

[kc_row use_container="yes" force="no" column_align="middle" video_mute="no" _id="384176"][kc_column width="12/12" video_mute="no" _id="145236"][kc_column_text _id="226528"]On Thursday, October 21, Total Accounting Care’s parent company - Stitely and Karstetter – will...

Safely Dispose of Old Documents and Sensitive Materials at Total Accounting Care’s Shredding Event on October 16

[kc_row use_container="yes" force="no" column_align="middle" video_mute="no" _id="144236"][kc_column width="12/12" video_mute="no" _id="207772"][kc_column_text css_custom="{`kc-css`:{}}" _id="282518"]Are boxes of old documents and sensitive materials cluttering up the...

Safely Dispose of Old Documents and Materials at Stitely and Karstetter’s October 16th Shredding Event

Are boxes of old documents and sensitive materials cluttering up the corners of your home or office space? Need a place to dispose of them safely? Then Stitely and Karstetter’s shredding event on Saturday, October 16 is just the solution you’ve been waiting for! Held...

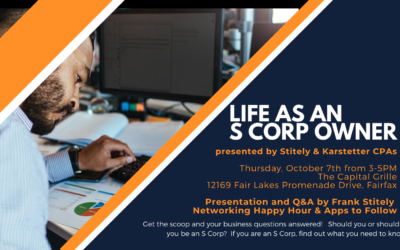

TAC’s Parent Company Sponsors October Networking Event – “Life as an S Corp Owner” Registration is Now Open

[kc_row use_container="yes" force="no" column_align="middle" video_mute="no" _id="569531" _collapse="1"][kc_column width="12/12" video_mute="no" _id="144880"][kc_column_text _id="14892"] Are you a business owner who is looking to learn more about becoming an S Corp?...

S&K Sponsors October Networking Event – “Life as an S Corp Owner” Registration is Now Open

Are you a business owner who is looking to learn more about becoming an S Corp? Then you won’t want to miss “Life as an S Corp Owner, ” an important networking event sponsored by SK CPAs & Business Advisors PLLC. The event is FREE and will be held at The Capital...

Pension Plans 101 – What You Need to Know

A pension plan is a type of retirement plan where employers promise to pay a defined benefit to employees for life after they retire. This is different from a defined contribution plan, like a 401(k), where employees put their own money in an...

There is Still Time to Claim Your Employee Retention Tax Credit

Eligible Businesses Can File Retroactive Claims for Wages Paid in Prior Tax Quarters On Aug. 4, the IRS issued further guidance on the employee retention credit, including guidance for employers who pay qualified wages after June 30, 2021, and before Jan. 1, 2022, and...

Stitely & Karstetter Sponsors October Networking Event – “Life as an S Corp Owner”

Are you a business owner who is looking to learn more about becoming an S Corp? Then you won’t want to miss SK CPAs & Business Advisors PLLC CPA’s upcoming networking event : “Life as an S Corp Owner. ” The event is FREE and will be held at The Capital Grill in...

CPA Q&A: Child Tax Credit

Now that July is here, many of our S&K clients who are full-time parents or caregivers to school-aged children, have begun receiving their Advance Child Tax Credit payments from the IRS. Most families will receive the first half of the credit in advance monthly...

Child Tax Credit Payments – How to Opt Out

On July 15, many of our TAC clients who are full-time parents or caregivers to school-aged children, began receiving their Advance Child Tax Credit payments from the IRS. The expanded child tax credit is part of the American Rescue Plan, signed by President Joe Biden...